Seeking Alpha and The Original Sin of Finance

Mexico’s $270 Billion Opportunity for Redemption

In Man’s Search for Meaning, Viktor Frankl describes a moment inside the concentration camp when everything familiar had already been stripped away, name, profession, dignity, future. What remained was hunger, cold, and the constant presence of death. And yet, Frankl noticed something unsettling: even there, in a place designed to annihilate meaning, some prisoners survived differently. Not because they were stronger, or smarter, or more optimistic, but because they found something to live for. A memory. A loved one. A sentence not yet written. In a world where suffering was unavoidable, meaning became the last form of freedom.

There is something inside every human being that searches for meaning. Aristotle believed we naturally move toward fulfillment, toward becoming what we already are in potential. Plato saw improvement as a longing for something lost, a faint memory of a more perfect reality. Hobbes reduced improvement to endless desire, motion without rest, while Schopenhauer argued that striving itself is the source of suffering: achievement only quiets the will for a moment before it demands more. Sartre reminded us there is no finished human essence, only perpetual becoming.

There is no place where this desire for improvement is more visible than in economics. Countries, as expressions of collective human will, seek improvement through GDP growth. Individuals seek it through alpha in capital markets.

Alpha is often described as outperforming the S&P 500, the most common yardstick of “average” market performance. But at its core, alpha is the quiet difference between keeping pace and pulling ahead. It is improvement over the standard, excess return earned not by chance, but by intention. In a world defined by averages, alpha is the choice to see more clearly, act more precisely, and achieve results that rise above what the market considers normal.

But between 1920 and 1930, an original sin was committed. Alpha, our ability to improve economically as individuals, was captured and locked away in the dark.

Before the Great Depression, there was little distinction between public and private investing from an access standpoint. Ordinary individuals invested directly in private partnerships, early-stage companies, real estate syndicates, and highly leveraged trusts. When the 1929 crash came, retail investors were wiped out, not just by stocks, but by opaque pooled vehicles they did not understand.

The regulatory response that followed, the creation of the SEC and the Investment Act of 1940 split markets in two. Public markets were designed for universal access and protection; private markets were reserved for those deemed capable of absorbing losses and complexity. Wealth became a crude proxy for sophistication. Over time, long-duration, compounding alpha concentrated inside private vehicles accessible mainly to institutions, family offices, and high-net-worth individuals.

As public markets became more efficient and returns more compressed, the restriction created a visible gap. Alpha was everywhere in conversation, but structurally inaccessible in practice. Our ability to improve was not eliminated, it was displaced.

Crypto, SPACs, meme stocks, NFTs, leveraged options: these functioned as synthetic private markets. Permissionless access to convex payoffs, early-stage narratives, and asymmetric upside, without gatekeepers. They replicated the emotional and payoff profile of venture investing, but without its positive-sum foundation or institutional safeguards.

The same logic explains the explosion of sports betting and other high-variance activities. When people are blocked from participating in productive, long-duration ownership, they migrate toward short-term variance, even when expected value is negative. Across crypto, betting, and speculative trading, the pattern is consistent: alpha denied does not disappear; it mutates.

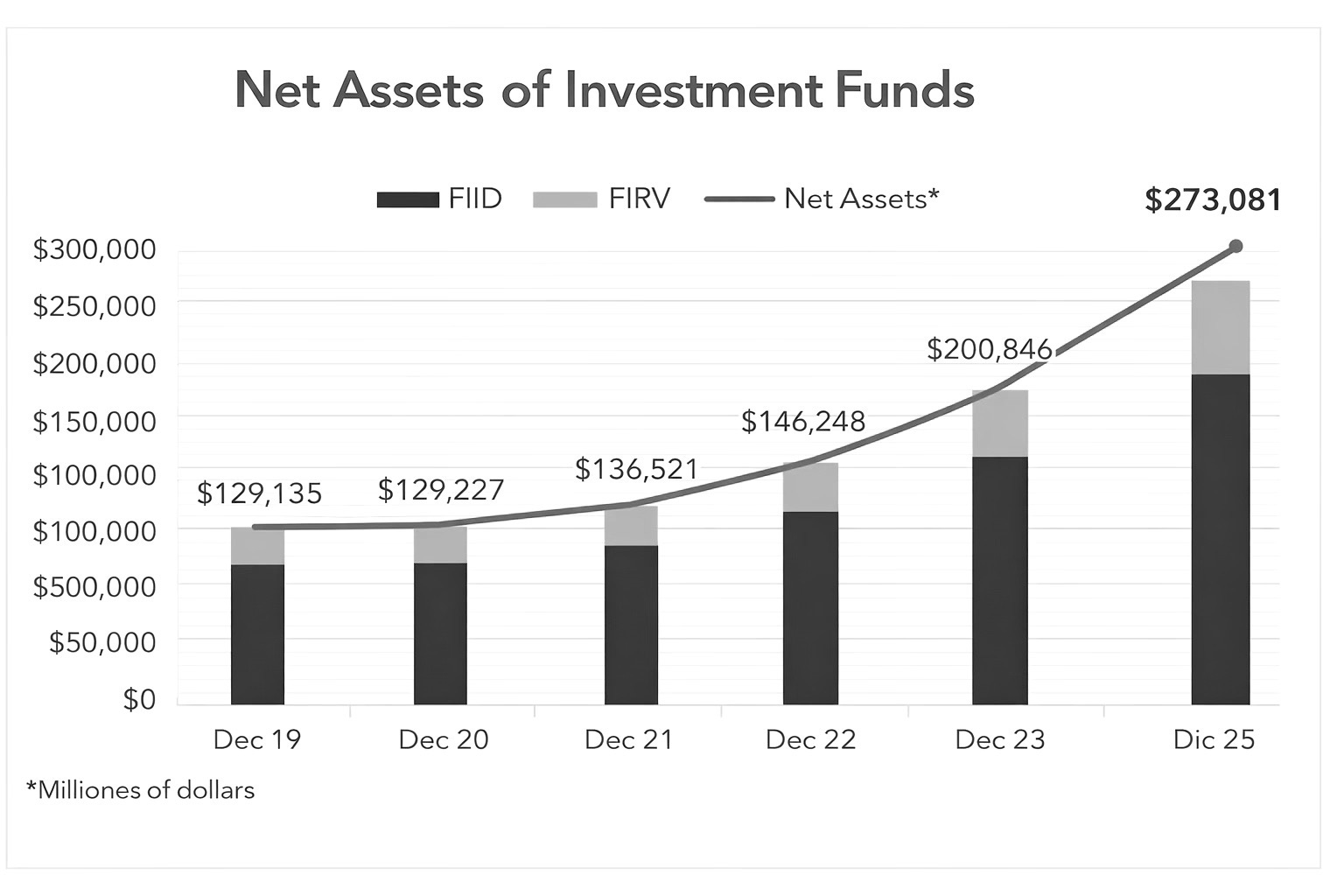

Nowhere is this more evident than in Mexico, Banks manage roughly $270 billion in assets, invested primarily in government debt and fixed-income products that, over time, have generated returns below the S&P 500, negative alpha. But the problem is not only low returns. The average Mexican investor pays active management fees for products that are effectively passive, a widespread practice of closet indexing. The result is a fee industry of nearly $4 billion, one of the largest revenue streams for Mexican banks, in which individual effort does not translate into progress, but into capture.

This brings us to our last philosopher. Byung-Chul Han names the pathology clearly: improvement has turned into self-exploitation. The tragedy is not that we seek to become better, but that we have forgotten what becoming was meant to serve.

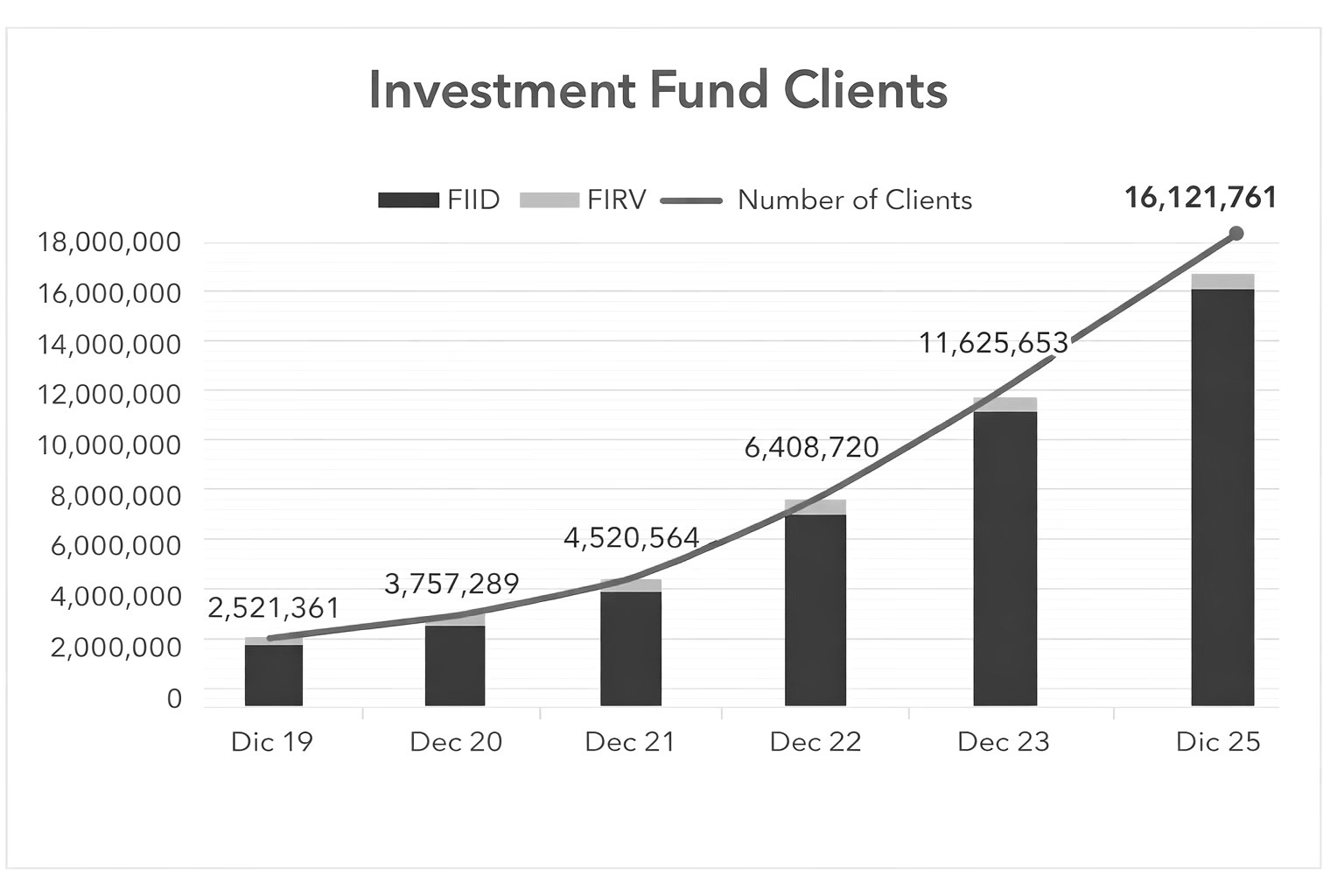

And yet, light is beginning to break through. Evergreen and semi-liquid funds are emerging and with that platforms are lowering minimums and expanding access to private markets. In Mexico alone, investment fund clients have grown from 3 million to more than 16 million in five years.

At Nazca, we are studying this shift closely. We believe society is approaching a moment of absolution, a chance to undo the original sin and recover something essential. As Viktor Frankl observed in the darkest conditions imaginable, freedom does not vanish when everything is taken away; it survives as the ability to choose what gives life meaning. Reclaiming alpha is not merely about outperforming a benchmark or the S&P 500. It is about refusing to let progress survive without purpose, and choosing meaning as a tool for freedom.